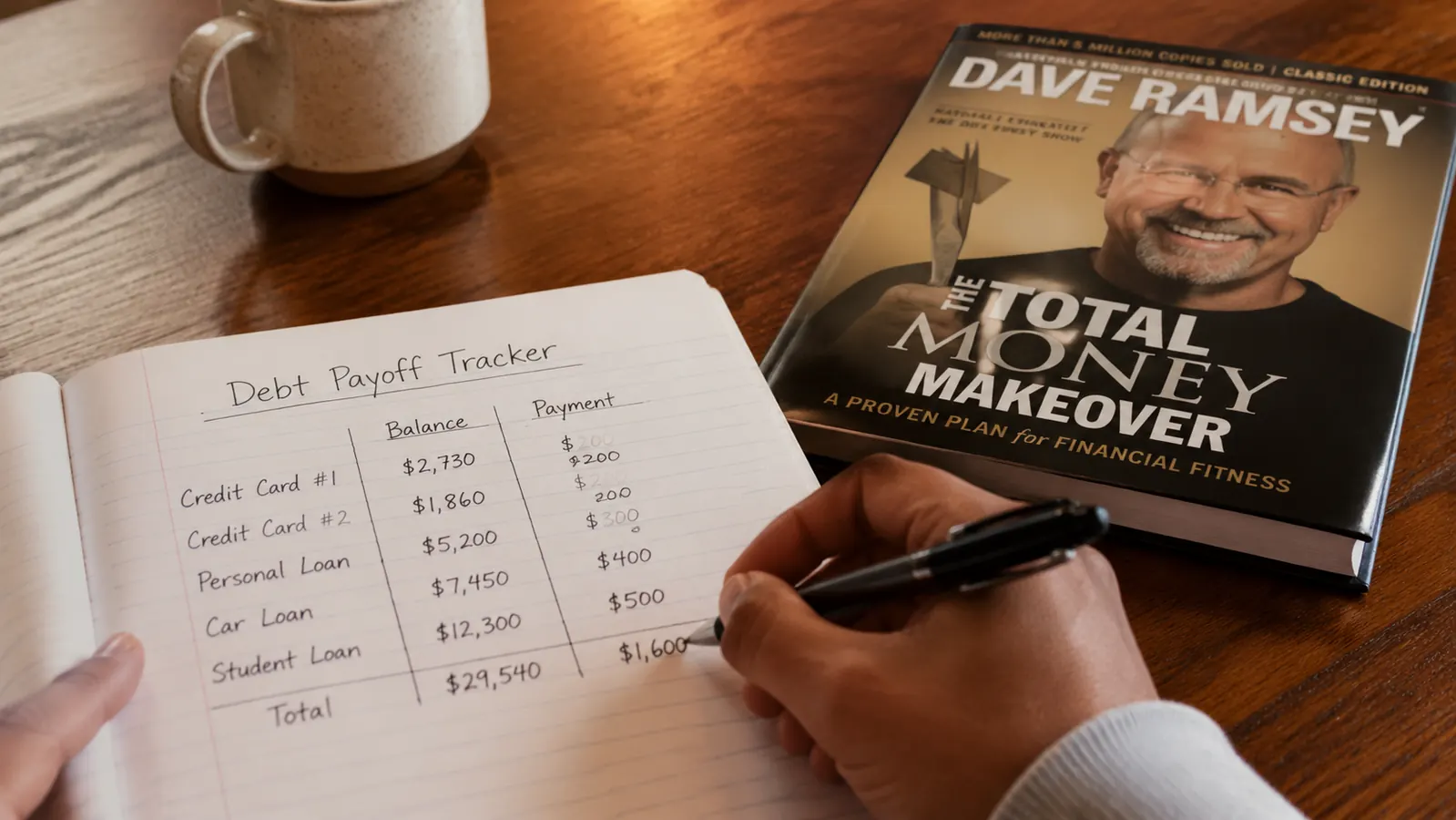

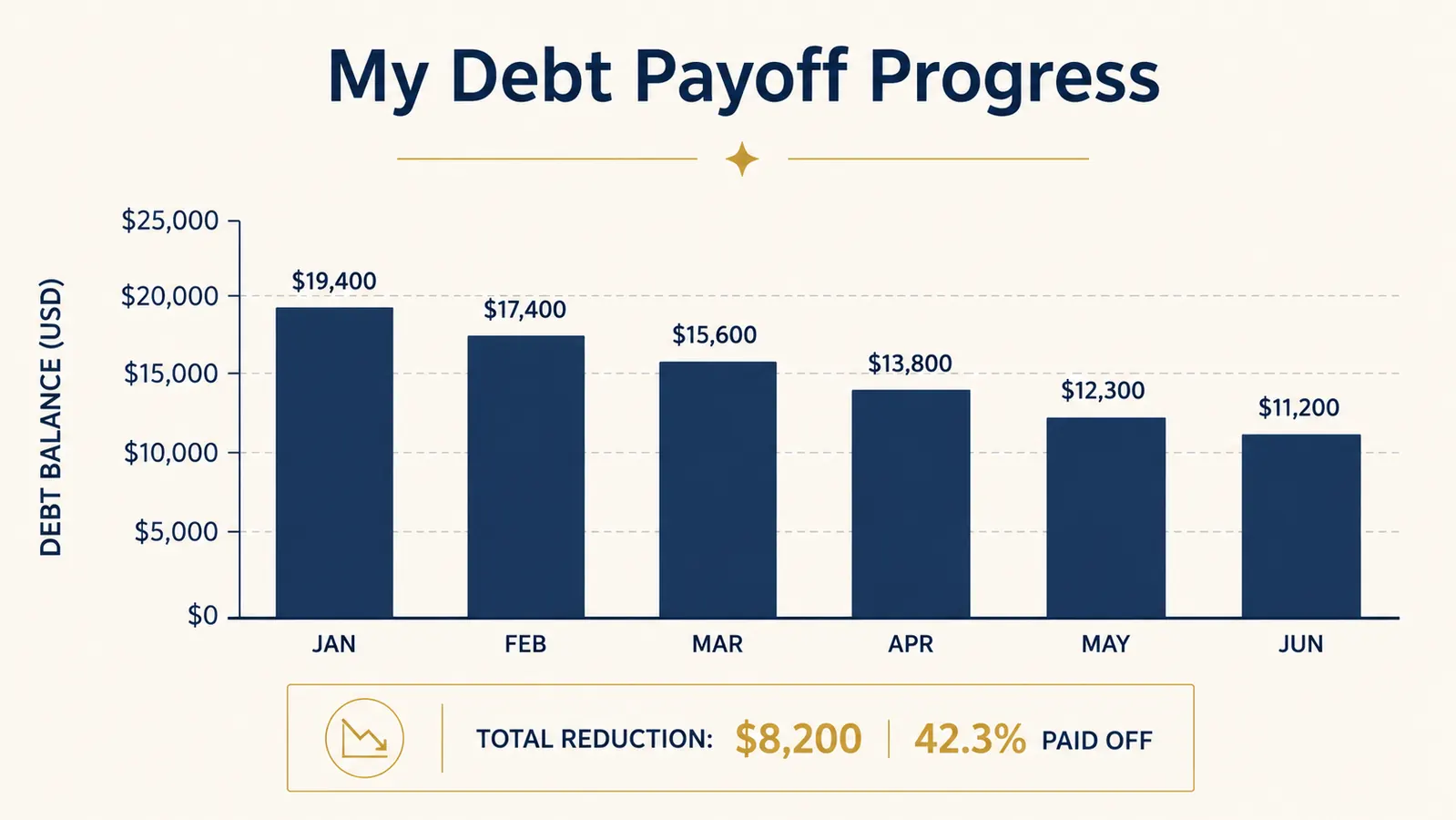

Last January I had $19,400 in debt across four credit cards and one personal loan. My minimum payments totaled $480 a month, and I was making just enough to cover them plus rent and groceries. My savings account had $214 in it. I had tried budgeting apps, YouTube rabbit holes, and a two-week phase where I wrote every purchase in a notebook. Nothing stuck. Then my coworker Marcus mentioned a book. He said he had used it to pay off $31,000 in about three years and that it was the first money advice he had ever actually followed to completion. I picked up a copy of The Total Money Makeover by Dave Ramsey that weekend. This review covers the six months I spent following it, including what changed, what did not, and where I think the book helps you and where it leaves you on your own.

I want to be clear about what this is: a real account from someone making $48,000 a year in a mid-size city, living alone, with no inheritance or side income to lean on. I followed the baby steps as written. I tracked every dollar. By the end of month six I had paid off two of my four debts completely and reduced my total balance from $19,400 to $11,200. I also built a $1,000 emergency fund in month one, which I had never had before. The book is the reason those two things happened.

The Quick Verdict

A no-nonsense, step-by-step plan that works if you are willing to stop budgeting by feel and follow a system. Not perfect, but it is the most actionable personal finance book I have read.

Amazon Check Today's Price →If you are tired of paying minimums and watching the balance barely move, this is where most people start turning it around.

The Total Money Makeover has over 22,000 reviews on Amazon. Pick it up, read Baby Step 1 and 2 in one sitting, and start your debt list that night. That is exactly what I did.

Amazon Check Today's Price on Amazon →How I Used It: Month by Month

I read the whole book in about four sittings over a long weekend. Ramsey's tone is direct, sometimes blunt, and at a couple of points he will make you wince if you have been doing the opposite of what he recommends. I appreciated that. I had read gentle, empathetic money books before. They made me feel understood and then I went right back to the same habits. This one felt like a friend who had been through it and was not going to let me off the hook.

Baby Step 1 is to save a $1,000 starter emergency fund before you do anything else. I finished that in about five weeks by cutting my grocery spending down to $180 a month (rice, beans, rotisserie chicken, lots of eggs), pausing my Spotify and gym membership, and picking up one Saturday shift a month at the coffee shop where I used to work part-time. I moved that $1,000 into a separate savings account and labeled it Emergency Only. I still have not touched it.

Baby Step 2 is the debt snowball: list all your debts from smallest balance to largest, pay minimums on everything, and throw every extra dollar at the smallest one until it is gone. Then roll that payment into the next one. My smallest debt was a $1,100 Best Buy card at 29% APR. I paid it off in six weeks. That moment felt different from anything a spreadsheet app had ever shown me. There is something about mailing (or clicking) a final payment on a debt that makes it real in a way a dashboard bar chart does not.

What the Book Gets Right

The debt snowball is the centerpiece of the book, and it works for a reason most financial people grudgingly admit: behavior beats math. From a pure interest rate standpoint, you should pay off the highest-rate debt first (the avalanche method). Ramsey does not tell you to do that, and he is correct not to. Most people who try the avalanche method quit before they see a debt fully eliminated. The snowball gives you a win early, and that win changes how you feel about your money. I felt it in my own house.

Ramsey is also right that budgeting is a prerequisite, not a supplement. The book spends a full chapter on zero-based budgeting, where every dollar of your income is assigned a job before the month starts. I had always budgeted loosely, tracking spending after the fact and feeling vaguely bad about it. Zero-based budgeting forced me to make decisions before I was in the grocery store or the drive-through. That shift in timing made a real difference. My discretionary spending dropped about 22% in the first month without me feeling especially deprived.

The book is also good on what Ramsey calls the wealth-building baby steps (steps 4 through 7), which cover investing 15% of your income into retirement accounts, saving for your kids' college, paying off your mortgage early, and building wealth to give. I am not at those steps yet, but reading them gave me a longer time horizon. When you are staring at credit card debt it is easy to feel like retirement savings is a luxury for people who have already figured things out. The book reframes that: the baby steps are designed to get you to wealth, not just to zero debt.

The debt snowball gave me a win in the first six weeks. I paid off a $1,100 card and then just sat there for a second. It sounds small, but that moment changed how I thought about the rest of it.

Where the Book Falls Short

The biggest gap for me was the income side. Ramsey focuses heavily on cutting spending and following the budget, but if your income is already close to bare-bones, the plan moves slowly. On $48,000 a year, after taxes and fixed expenses, I had about $400 a month to throw at debt beyond minimums. That is enough to make real progress, but it means paying off $19,400 takes years, not months. Ramsey does address increasing income but in fairly brief terms. He suggests picking up extra work, selling things, and being intense about it. That advice is true but not very specific for someone who has already maxed out their hours at one job.

The book also reflects a worldview that does not always translate for people in higher cost-of-living cities. Ramsey's examples often assume you can cut a gym membership and suddenly redirect $80 a month to debt, which works in a lot of places but means less in a city where your rent alone is 45% of take-home pay. He does not really address that tension. I found myself making adjustments and improvising rather than following the plan as written in those areas.

One more thing worth naming: the book's position on credit cards is absolute. Ramsey believes you should cut them up and never use them again. I understand the argument, and for someone with a history of running up balances it makes sense. But for someone who is disciplined and would lose cashback rewards and fraud protection by eliminating cards entirely, the no-exceptions stance can feel more ideological than practical. You can follow the debt snowball and zero-based budget without necessarily agreeing with every opinion in the book.

How It Compares to Other Books I Have Tried

I read two other personal finance books in the year before picking up the Total Money Makeover. I will not name them because they were not bad books, but they were heavy on mindset and light on mechanics. By the time I finished them I felt motivated but did not know what to do on Monday morning. The Total Money Makeover is the opposite. By the end of chapter three you have a list of your debts and a plan for the next paycheck. I think that specificity is the reason it has sold over five million copies.

If you want to understand the psychology behind your money decisions, Morgan Housel's The Psychology of Money is a better read. But if you want a concrete system to follow, Ramsey wins by a wide margin. I wrote a full comparison of both books if you want to see them side by side: Total Money Makeover vs The Psychology of Money. The short version: read the Total Money Makeover first, then read Housel when you are ready to think longer term.

I also want to mention that the baby steps pair naturally with physical budgeting tools. I started using a cash envelope system in month two and it made the zero-based budget easier to maintain in real life. If you are curious about that approach, the reasons the Dave Ramsey budget plan works article goes into the mechanics of that setup in more detail.

Six-Month Results, By the Numbers

Here is what actually changed between January and the end of June. I started with $19,400 in total debt across five accounts. I finished with $11,200 across three accounts. The Best Buy card ($1,100) and an old medical bill ($2,600) are both gone. My credit card minimums dropped from $480 per month to $290 per month because two balances are at zero. My starter emergency fund has sat at $1,000 the entire time, untouched. And for the first time since I started working full time, I have not added to my debt in six months. Every month has been net positive.

Those numbers are not dramatic. Some people on Ramsey's radio show call in and report paying off $90,000 in 18 months, usually with a spouse and a combined income above six figures. My situation is different. But $8,200 in net debt reduction in six months is real progress I had never managed before. The book is why I have a system. Having a system is why I have the results.

What I Liked

- The debt snowball method is genuinely effective at keeping you motivated through a multi-year payoff

- Zero-based budgeting forces decisions before spending, not after, that timing shift matters

- The baby steps give you a complete roadmap from zero savings to investing and wealth building

- Written in plain language with no financial jargon, anyone can follow it

- With over 22,000 reviews and 4.7 stars, it has a proven track record across a wide range of incomes and situations

Where It Falls Short

- Income-side advice is limited, if you are already stretched thin, the pace of the plan depends almost entirely on cutting spending

- The no-credit-card-ever stance is more absolute than it needs to be for disciplined users

- High cost-of-living cities are not well addressed, the examples skew toward situations where cutting a few bills moves the needle more

- Some sections feel repetitive, especially the motivational chapters, the practical content could be condensed

Who This Is For

The Total Money Makeover is best suited for someone who knows they are stuck but does not have a plan. If you have debt, feel like you are treading water every month, and have tried to budget before but never stuck with it, this book was written for you. It works best when you commit to following the baby steps in order and do not skip ahead. It also works better for people who are motivated by clear rules and concrete checklists than for people who need a lot of flexibility and nuance. If you are a rules person, you will love it. If you are more of a systems thinker who likes to weigh tradeoffs, some of the book's black-and-white stances will chafe a little.

Who Should Skip It

If you are already debt-free and looking for investing advice, this is not your next read. The wealth-building sections are introductory and Ramsey will point you toward his other resources rather than go deep on portfolio strategy. If your financial situation is complex (self-employment income, divorce, bankruptcy, or irregular seasonal income), the baby steps are a reasonable framework but you will need supplementary guidance for the specifics. And if you strongly disagree with Ramsey's religious framing, which appears occasionally throughout the book, it may distract from the practical content enough to be worth knowing about before you buy.

Six months and $8,200 in debt gone. It started with reading Baby Steps 1 and 2 in one weekend.

The Total Money Makeover is consistently one of the best-reviewed personal finance books on Amazon. If you have been meaning to get your finances in order and keep putting it off, picking this up is the most useful $13 you can spend on the problem.

Amazon Check Today's Price on Amazon →