I did freelance work on the side for three years before someone finally told me I was probably overpaying on taxes. I thought my situation was too simple to have many deductions. I worked from my spare bedroom, drove to client meetings, bought a new laptop, and paid for a couple of software subscriptions. Turned out every one of those things could qualify as a deduction under IRS rules. I just never knew to ask, until a worn copy of 475 Tax Deductions for Businesses and Self-Employed Individuals showed me how much I had been leaving on the table.

Freelancers and gig workers get hit harder by taxes than traditional employees for one simple reason: no employer is withholding on your behalf or covering half your self-employment tax. You owe both sides of Social Security and Medicare yourself, which adds up fast. The way you offset that burden is by claiming every legitimate deduction you qualify for. Most people do not do this because nobody ever walked them through it. That is what this guide is for. And as always, what is here is a starting point, not tax advice. Before you file, confirm your specific situation with a tax professional or check current IRS guidance at IRS.gov, because the rules do change.

If you do gig work or freelance even part time, you are probably missing deductions right now.

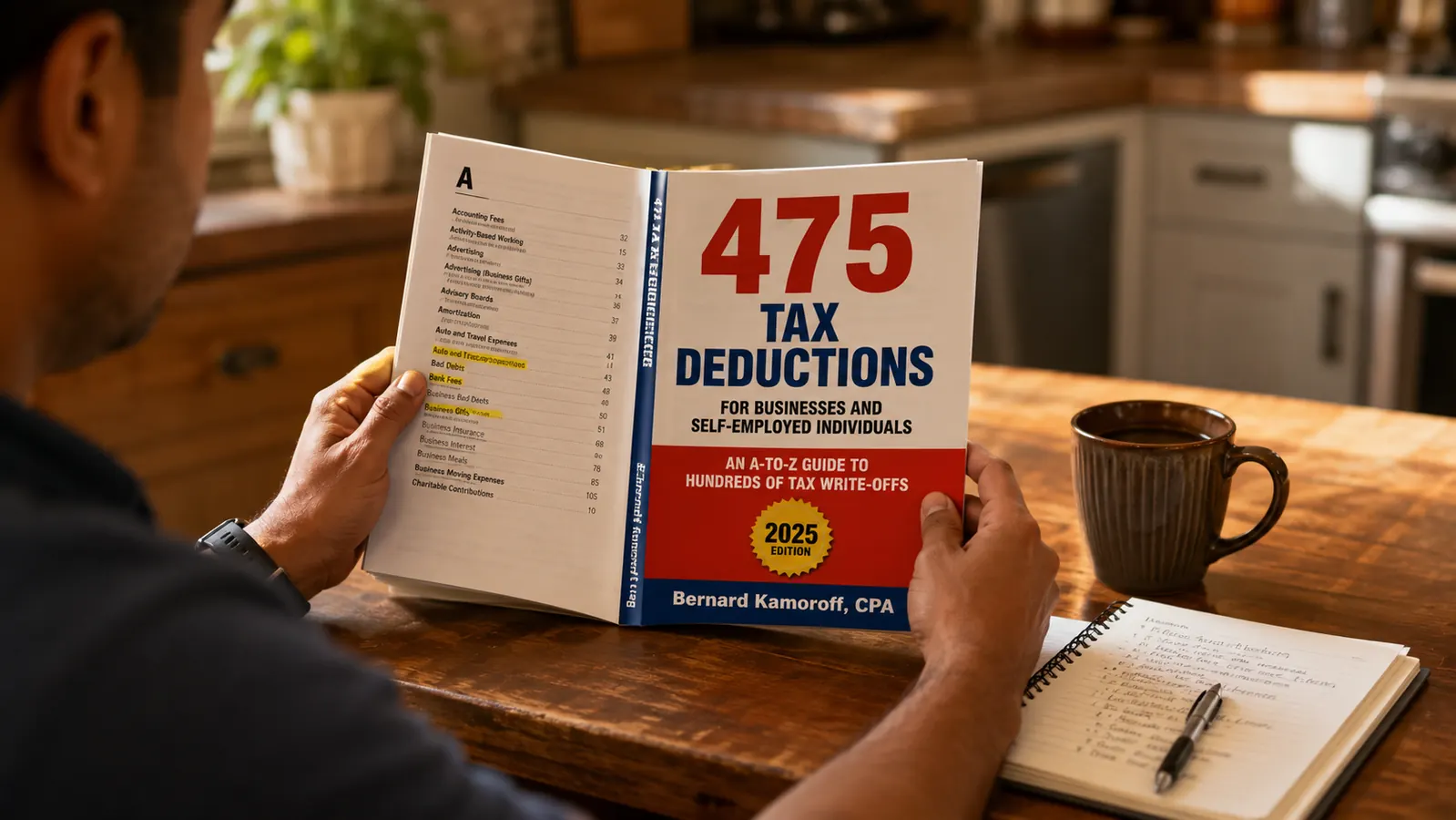

The 475 Tax Deductions for Businesses and Self-Employed Individuals book by Bernard B. Kamoroff is a plain-English A-to-Z reference covering hundreds of write-offs that apply to self-employed people. It has a 4.7-star rating from over 1,300 verified buyers and it is the resource I keep on my desk every January.

Amazon Check Today's Price on Amazon →Step 1: Separate Your Business Activity From Your Personal Life on Paper

Before you can claim anything, you need a clear record that the expense was for your freelance work and not your personal life. The IRS standard is that an expense must be both ordinary (common in your line of work) and necessary (helpful and appropriate for your business). You do not need a separate LLC or a formal business entity to qualify. If you earned income from gig work, you are already self-employed in the eyes of the IRS, and that means Schedule C applies to you.

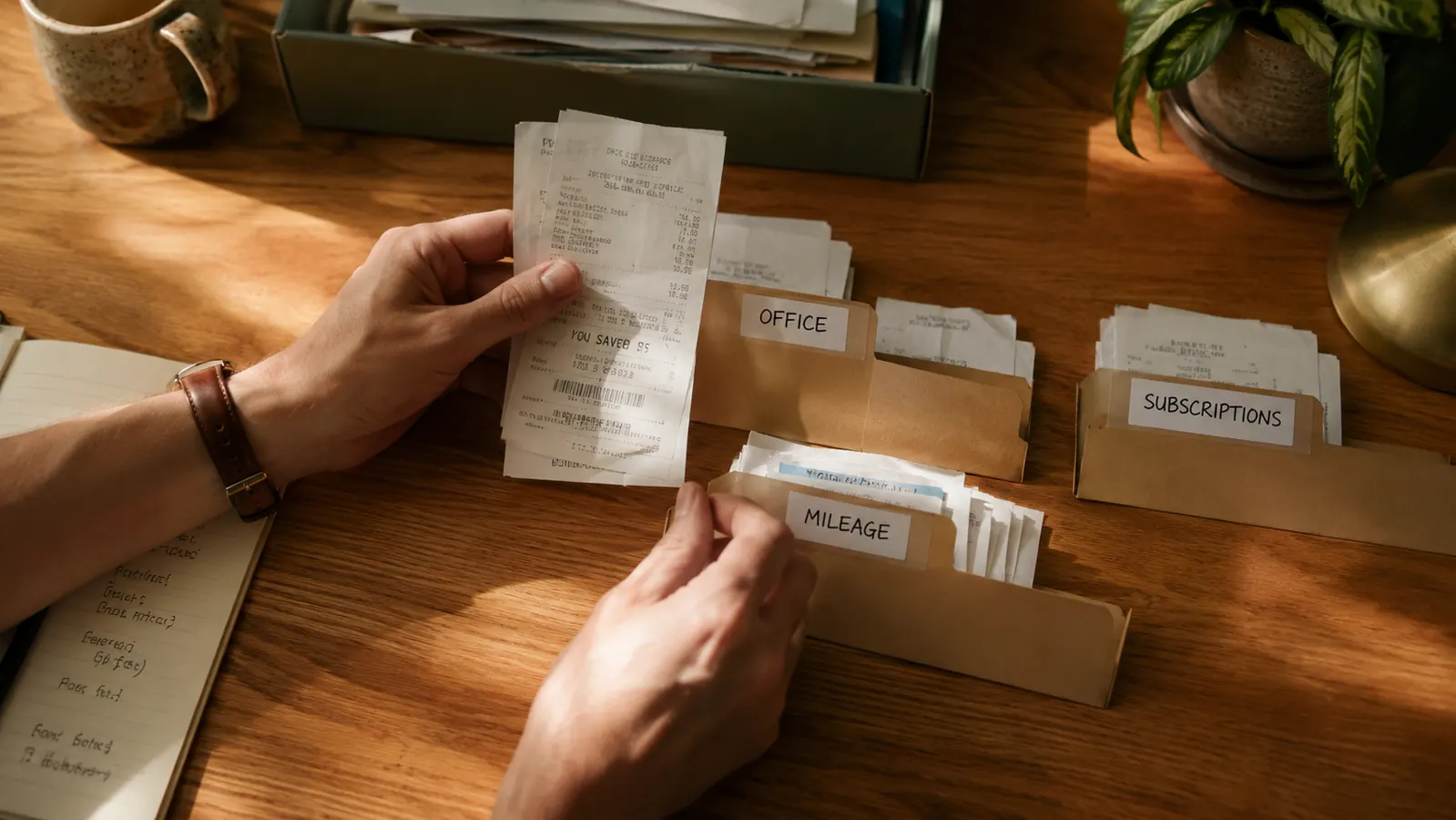

Open a dedicated checking account or at minimum a separate credit card for all business purchases, even if your business is just a weekend side hustle. This is the single best habit you can build. When everything mixes together in one account, you end up spending hours at tax time guessing which charges were work-related, and you almost always miss something. When business spending is in its own column, the list of potential deductions basically writes itself.

Even if you did not do this last year, you can still reconstruct your expenses by going through bank and credit card statements month by month. It takes a Saturday afternoon, but it is worth the effort. Highlight anything that was clearly for your freelance work, note the business purpose on a sticky note or spreadsheet, and save the backup documentation. A short memo to yourself counts as a record. You do not need a formal receipt for every small purchase, though having one is always better.

Step 2: Walk Through the Home Office Deduction Carefully

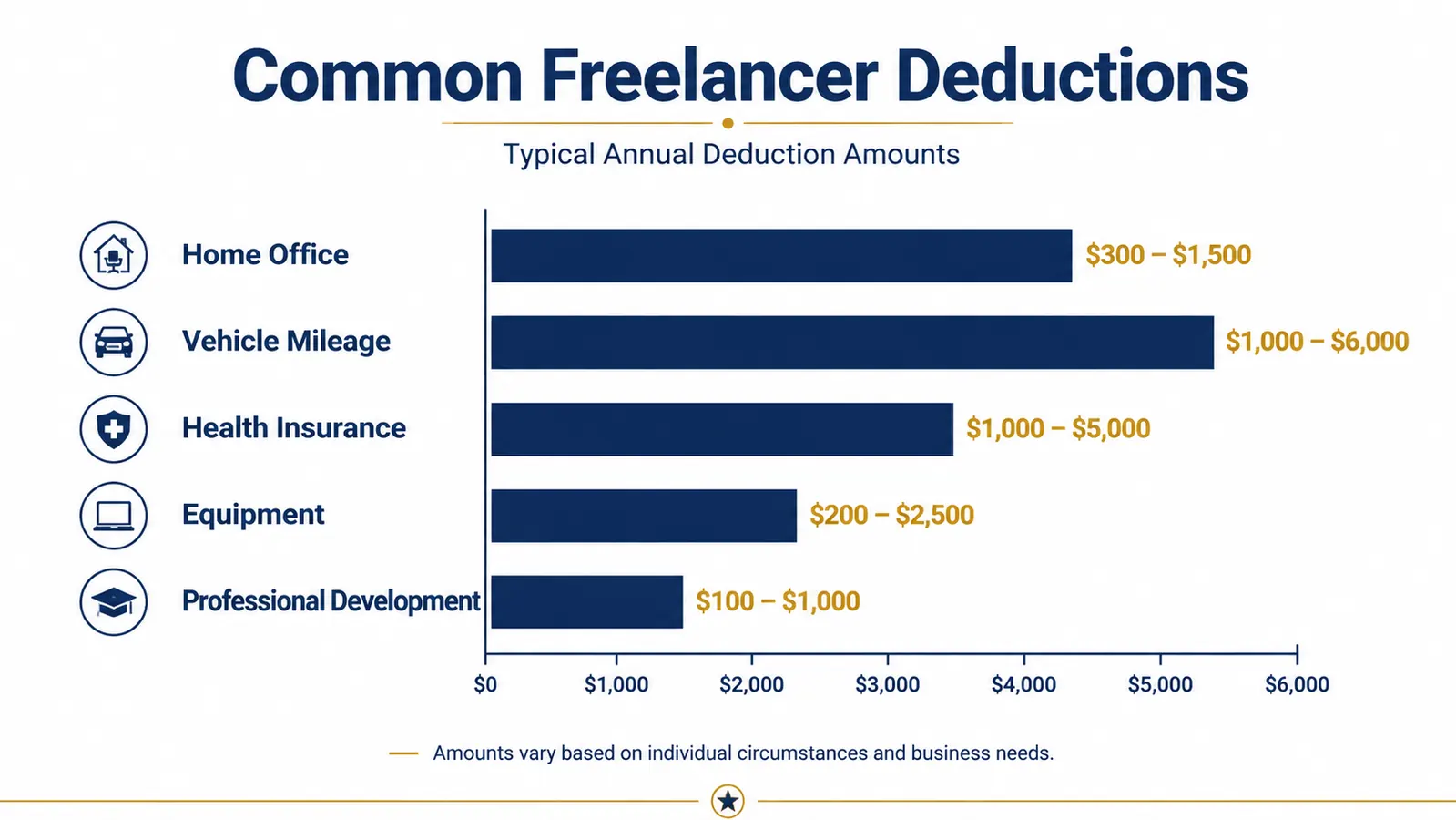

If you work from home, you may be able to deduct a portion of your rent or mortgage interest, utilities, internet, and home insurance based on the percentage of your home used exclusively and regularly for business. The keyword there is 'exclusively.' A spare bedroom that doubles as a guest room likely does not qualify. A dedicated room used only for client calls and project work almost certainly does. The IRS has a simplified method that lets you deduct five dollars per square foot, up to 300 square feet, without tracking every utility bill. For most freelancers just starting out, that simplified method is the easier route.

It is worth reading the IRS guidance on the home office deduction directly, because the rules have a few conditions that trip people up. Publication 587 on IRS.gov covers the home office deduction in plain language, and it is free. Your situation may qualify in ways you have not considered, or it may have a wrinkle that makes part of it more complicated. A tax professional who works with self-employed clients can run the numbers both ways and tell you which method saves you more.

Step 3: Account for Every Mile You Drove for Work

Vehicle mileage is one of the most commonly missed deductions for gig workers, especially people who do delivery, rideshare, or client-site work. The IRS publishes a standard mileage rate each year (check IRS.gov for the current rate, since it adjusts periodically), and you can use that rate times the number of business miles you drove to calculate your deduction. If you drove 8,000 miles for work in a year, even at a modest rate, you are looking at a real deduction that could meaningfully lower your taxable income.

The catch is documentation. You need a mileage log that records the date, destination, business purpose, and number of miles for each trip. There are free apps that do this automatically, like MileIQ and Everlance, or you can keep a small notebook in your car. If you did not track miles in real time, you can often reconstruct them from Google Maps history, calendar appointments, or gig platform records. The important thing is to have something written down that shows the business purpose of each trip. Driving to pick up office supplies counts. Driving to a client site counts. Commuting to a location you work at regularly is generally not deductible, so check the IRS guidance if you are unsure where your situation falls.

Step 4: List Every Tool, Software, and Subscription You Used for Work

Equipment and supplies you buy for your business are generally deductible. That laptop you use for freelance projects, the external hard drive for backing up client files, the ring light for video calls, the desk chair you bought to work from home, the design software subscription, the project management tool, the accounting app. If it is something you use in the course of doing your work, it belongs on your list. The IRS allows you to deduct the full cost of many business assets in the year you buy them under Section 179, rather than depreciating them over several years. That can make a big difference in your tax bill the year of the purchase.

Do not forget ongoing subscriptions. Adobe Creative Cloud, Canva Pro, Zoom, Grammarly, QuickBooks Self-Employed, Notion, Dropbox, even your professional LinkedIn subscription if you use it to find clients. These are ordinary and necessary expenses for most freelancers and they add up over twelve months in ways that are easy to overlook when you pay monthly and forget about it. Pull your bank statement and go line by line. You will likely find three or four subscriptions you forgot you were even paying for that are fully deductible.

Step 5: Look at Deductions Specific to Self-Employed People That Employees Never Get

There are a handful of deductions that are unique to self-employed workers and can meaningfully reduce your tax burden. The self-employed health insurance deduction lets you deduct premiums you pay for health, dental, and vision coverage for yourself and your family, directly off your adjusted gross income, not just as an itemized deduction. If you pay for your own insurance because you do not have an employer plan, this one can be substantial. The deduction for half of your self-employment tax is another one that most gig workers do not realize exists. Because you are paying both the employee and employer share of Social Security and Medicare, the IRS lets you deduct the employer half as a business expense.

Retirement contributions are a third category worth knowing about. A SEP-IRA or a Solo 401(k) lets self-employed people put away a significant portion of their net self-employment income before taxes, which reduces taxable income now while building savings for later. The contribution limits are considerably higher than a standard IRA, and the setup is simpler than most people expect. A fee-only financial planner or a CPA who works with freelancers can show you exactly how much you could contribute based on your net income for the year. This is one of those areas where a professional consultation often pays for itself many times over.

What Else Helps

Having a structured reference you can turn to throughout the year makes a bigger difference than most people expect. Tax code is dense and changes frequently. When you are building a deduction checklist for the first time, starting from scratch means you will inevitably miss categories that apply to you. The 475 Tax Deductions for Businesses and Self-Employed Individuals book by Bernard B. Kamoroff is one of the most practical tools I have found for this. It is organized alphabetically so you can look up any expense you are wondering about and see exactly what the deductibility rules are, what documentation you need, and where it goes on your return. It is written for people who are not accountants, which matters when you are trying to figure things out at 10 p.m. before a filing deadline.

Beyond the book, consider working with a CPA or enrolled agent who specializes in self-employed clients at least once, even if you normally file your own return. Many freelancers find that a single session with a professional reveals two or three deductions they had never claimed, and those savings can more than cover the cost of the consultation. The IRS Free File program also offers free guided filing for taxpayers below certain income thresholds. And if you want to dig into the rules yourself, IRS.gov has detailed publications on every topic covered in this guide, all free and legally authoritative.

For more on which specific deductions freelancers miss most often, the article on the ten tax deductions most people miss walks through a concrete list. If you want a deeper look at how the 475 Tax Deductions book holds up over multiple filing seasons, the long-term review covers that in detail.

The goal is not to be clever about taxes. It is to claim what you legally qualify for and not leave your own money sitting on the table because nobody told you it was there.

A reference book that lists every deduction you qualify for is worth keeping on your desk every January.

The 475 Tax Deductions for Businesses and Self-Employed Individuals by Bernard B. Kamoroff covers hundreds of write-offs in plain, alphabetized format. It is one of the most practical tools available for freelancers and gig workers who want to stop guessing about what they can claim. Over 1,300 verified buyers give it a 4.7-star rating.

Amazon Check Today's Price on Amazon →