I spent two years trying to budget with apps. I had Mint, then Every Dollar, then a color-coded spreadsheet my coworker swore by. Every month I would start strong and by the third week I would open the app, see a red number, close it, and decide to try again next month. The money was still leaving my account. I just stopped looking at where it went.

The thing that finally worked for me was the dumbest-sounding solution: I started using cash. Not because cash is magic, but because when the envelope is empty, you can see it is empty. There is no app to close. That physical feedback is what changed my behavior. The SKYDUE Budget Binder gave me the right container to make that system work. It has labeled zipper envelopes, expense tracking sheets, and budget worksheets all in one compact binder that fits in a purse or laptop bag. Here is exactly how I set it up, step by step, so you can do the same thing this weekend.

The binder that finally made budgeting feel real, not just something I planned to do.

The SKYDUE Budget Binder comes with zipper envelopes, budget sheets, and expense trackers. Rated 4.7 stars across more than 19,000 reviews. Check current pricing on Amazon before you read another step.

Amazon Check Today's Price on Amazon →Step 1: List Every Source of Income You Bring In Each Month

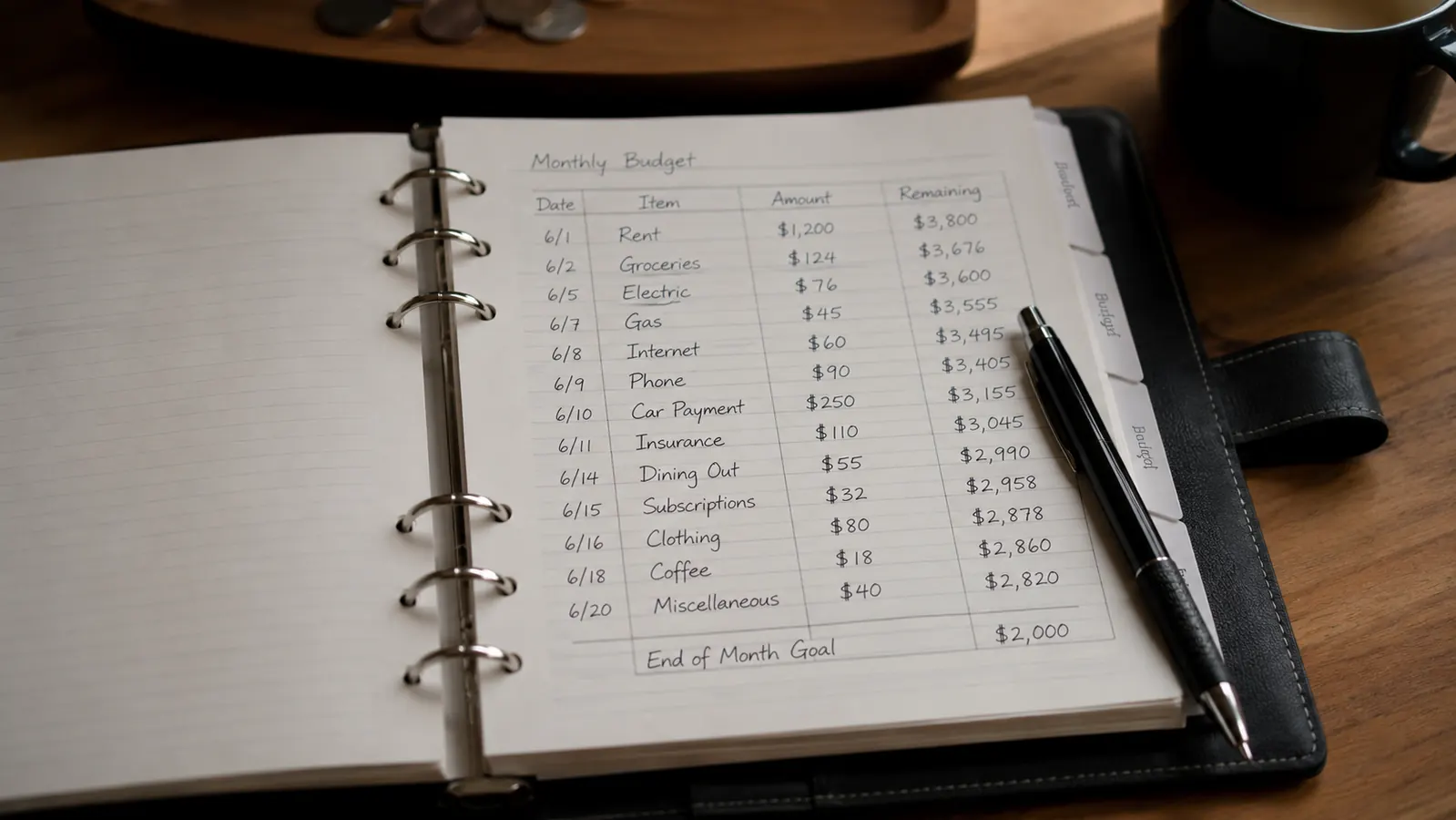

Before you touch the envelopes, you need one number: your actual take-home pay. Not what you earn on paper. What actually hits your bank account after taxes, insurance deductions, and anything else that comes out before you see it. If you get paid twice a month, add both checks. If your income varies, use your lowest recent month as your baseline so you are never planning with money that might not show up.

Write this number at the top of one of the budget worksheets that comes in the SKYDUE binder. Every category you fund in the next step has to come out of this number. Having it written in front of you makes the math feel concrete rather than abstract. Most people skip this step and wonder why their envelopes run out too fast. They were budgeting based on a vague sense of what they earn, not the real number.

If you have a partner who contributes to household expenses, add their take-home too and list it as a separate line so you can see where each amount comes from. Keep this worksheet in the first sleeve of the binder so it is the first thing you see when you open it.

Step 2: Set a Dollar Amount for Each Budget Category

Now divide that income across your spending categories. The SKYDUE binder comes with pre-printed budget sheets that already list common categories: groceries, utilities, gas, dining out, entertainment, clothing, medical, personal care, savings, and a few blank ones for anything specific to your life. Go through each one and write in how much you plan to spend there this month.

The rule is simple: your category totals cannot exceed your take-home income from Step 1. If they do, you have to reduce something. There is no borrowing from next month, no carrying a balance. This constraint feels harsh at first but it is actually the whole point. It forces a real conversation with yourself about what matters. Groceries for a family of four might need $600. Dining out might need to come down to $80 for now. That is not forever. It is just this month.

A good starting point if you have no idea what you spend: look at your last two bank statements and add up what you actually spent in each category. Use that as your baseline, then shave 10 percent off anything that surprised you. You do not have to be perfect. You just have to start with numbers that are close enough to be useful.

Step 3: Label the Envelopes and Load the Binder

The SKYDUE binder comes with multiple zipper envelopes and tab dividers. Take each envelope and write your category name on the label area, or use a small sticky label if you want it to look neat. One envelope per category that you plan to spend from in cash. You do not need an envelope for fixed bills you pay online, like your rent or car payment. Those are automatic. The envelopes are for the variable spending where you tend to go over budget: groceries, gas, eating out, personal care, fun money.

Slot each labeled envelope into the binder behind its corresponding tab. The binder holds them snugly so nothing falls out even if you toss it in your bag. Keep the expense tracking sheets behind each envelope so you can log what you spend right when you spend it, not later from memory when the details blur together.

Step 4: Withdraw the Cash and Fill the Envelopes on Payday

This step is the one that feels weird until it becomes a ritual. On payday, go to the ATM or your bank and withdraw the total of all your cash categories. If groceries is $500, gas is $120, dining is $80, personal care is $60, and fun money is $50, you withdraw $810. Ask the teller if you want specific bills. Twenties work fine for most envelopes, but having some tens and fives for smaller categories like personal care makes it easier to keep track.

When you get home, sit down with the binder and count out the right amount into each envelope. Seal each one and write the starting balance on the expense sheet. This whole process takes about ten minutes. I do it every other Friday morning with a cup of coffee. It is oddly satisfying, like packing your gym bag the night before. You are setting yourself up to make the right choice without having to think about it in the moment.

If you are paid on an irregular schedule, pick one day a week to be your unofficial payday and move money from your checking account to your cash stash on that day. The system works the same way regardless of when income arrives, as long as you are pre-funding the envelopes before you start spending.

Step 5: Track Every Purchase and Adjust as You Go

Every time you spend from an envelope, write it down on the expense sheet inside that envelope. Date, what it was for, amount spent, remaining balance. This sounds tedious. In practice it takes fifteen seconds per transaction. The act of writing it reinforces the decision in a way that tapping a card never does. By mid-month you will have a clear picture of what is left in each category and whether you need to slow down or whether you have some breathing room.

When an envelope hits zero, that category is done for the month. If you need to buy groceries and the grocery envelope is empty, the only way to do it is to take money from another envelope and mark that you are doing it. That visible trade-off, deciding to pull from fun money to cover groceries, is what makes the system honest. It forces a decision every time rather than letting spending just accumulate invisibly until you check the app at the end of the month and feel bad.

At the end of the month, whatever is left in each envelope is real money you did not spend. You can roll it into next month's same category as a buffer, move it to your savings envelope, or use it to make a small extra debt payment. This is where the system starts compounding. My first month using the SKYDUE binder I had $47 left over across all envelopes. It is not a big number. But it was the first time in years I had anything left over at all.

What Else Helps When You Are Getting Started

The binder handles the physical system well, but a few habits make it stick. First, carry the binder with you. It is compact enough to fit in most bags. If you leave it at home, you will default to your card because it is what you have on you. The whole point is that the envelope is the decision-maker, not you in the moment at the checkout counter.

Second, give yourself a small cash category you do not have to explain to yourself. Call it Fun Money or Personal. Put a modest amount in it, maybe $30 or $50, and spend it on whatever you want without logging the details. Having that guilt-free category makes the rest of the budget feel less like punishment. People who try to track every dollar with zero flex almost always quit within six weeks.

Third, look at the binder regularly, not just on payday. I open mine every Sunday evening for about five minutes. I check where each envelope stands, adjust my plan for the coming week, and make sure nothing is going sideways. That weekly check-in is when the system goes from a one-time setup to an actual habit. The SKYDUE binder makes this easy because everything is in one place: the envelopes, the tracking sheets, and the original budget worksheet you filled out at the start of the month. You do not have to reconstruct anything. You just open it and read.

If you want more structure around the overall debt-payoff or savings picture, pairing this system with a book like our full SKYDUE review gives you context on how other people have used it long-term. And if you are wondering whether the cash envelope approach is right for you before committing, this breakdown of why cash envelopes work covers the behavioral research in plain language.

The first month I used it I had $47 left over across all my envelopes. It is not a life-changing number. But it was the first time in years I had anything left at the end of the month at all.

If every app has let you down, try a system that works in your hands, not on a screen.

The SKYDUE Budget Binder has zipper envelopes, expense tracking sheets, and budget worksheets all in one compact binder. Rated 4.7 stars across more than 19,000 Amazon reviews. See today's price before your next payday.

Amazon Check Today's Price on Amazon →