My brother Marcus Jr. had been telling me to read The Little Book of Common Sense Investing for two solid years. He would bring it up at Thanksgiving, text me about it after a market drop, mention it whenever I complained about not knowing where to put my money. I am Marcus Sr., 38, warehouse supervisor, and I kept pushing it off because I figured if the advice was that simple the book probably was not worth reading. Last winter I finally picked it up. And here is the honest version of what I found: my brother was mostly right, and also missing a few things he forgot to mention.

I want to give you the fair read on this book because most reviews land in one of two camps. Either someone tells you it changed their entire financial life, or someone tells you it is just a long advertisement for Vanguard. Both of those framings skip the more useful truth, which is that this book does one specific thing very well, has some real limitations, and is right for a specific kind of person but not for everyone who picks it up.

The Quick Verdict

Bogle makes an airtight case for low-cost index funds and then makes it again, and again. The core argument is correct and worth absorbing. But the repetition is real, the examples skew toward 1990s fund data, and it leaves you with the why but not the how. Still worth reading. Just know what you are getting.

Amazon Check Today's Price →If your 401k has funds you picked without knowing the expense ratios, this book will change how you look at that statement.

The Little Book of Common Sense Investing by John C. Bogle has over 11,000 Amazon ratings. It is a short book with a persistent argument that holds up. Check today's price before you decide.

Amazon Check Today's Price on Amazon →What I Actually Read and How I Read It

I read the 10th anniversary edition over three evenings in January. I had a notepad, I highlighted passages, and I came in skeptical. I am not a finance person by training. I have a 401k through work that I have never paid close attention to, a small amount in a savings account, and the general sense that I am behind where I should be at 38. I have tried picking stocks exactly once, lost about $300 in three months, and decided I was not cut out for it.

The book opens with Bogle's core argument: stock market investing is a zero-sum game before costs and a loser's game after them. Meaning, for every investor who beats the market, another investor underperforms it by the same amount. Add in the fees that active fund managers charge, and the math tilts against you before you even start. The solution Bogle proposes is to stop trying to beat the market and instead buy the whole market through a low-cost index fund, then hold it for as long as possible. That is the argument. He makes it clearly in the first three chapters. Then he spends the next 18 chapters making it again with different data.

That repetition is something I want to address directly because nobody warned me about it. The book is 216 pages but the payload is closer to 40. If you are a fast reader who absorbs an argument the first time through, you will hit chapter 6 and start wondering whether you missed something because the book keeps circling back to the same point. You did not miss anything. That is just how the book is structured.

The Repetition Problem Nobody Talks About

I counted. The phrase or concept of 'tyranny of compounding costs' appears in roughly eight chapters. The chart showing long-run fund underperformance versus the index shows up in multiple variations. Bogle introduces a new set of historical mutual fund data, runs the same calculation showing active funds trail the index after fees, and arrives at the same conclusion. Then the next chapter does it again with a different fund category.

This is not necessarily a flaw in the argument. Bogle is building a cumulative case, and there is something to be said for seeing the same principle hold across small-cap funds, bond funds, international funds, and balanced funds. But if you are reading this primarily to decide whether to open an index fund account and what kind to open, chapters 8 through 14 will test your patience. I skipped two of them entirely and did not feel like I missed anything when I hit the final chapter.

The practical move: read chapters 1 through 7 carefully. Skim 8 through 14. Come back for the final two chapters, which contain the clearest summary of what to actually do. You will get 90 percent of the value in half the time.

The Dated Examples and What That Means for You

A second thing worth flagging is that a meaningful portion of the book's supporting data comes from the 1970s, 1980s, and 1990s. Bogle uses fund performance records going back decades to show that active management has historically underperformed index funds. That historical record is real and the data holds up. But a reader in their 30s looking at their own situation in 2026 will notice that the specific funds he references, the specific managers he critiques, and the specific market conditions he describes belong to a world that looked quite different from today's brokerage landscape.

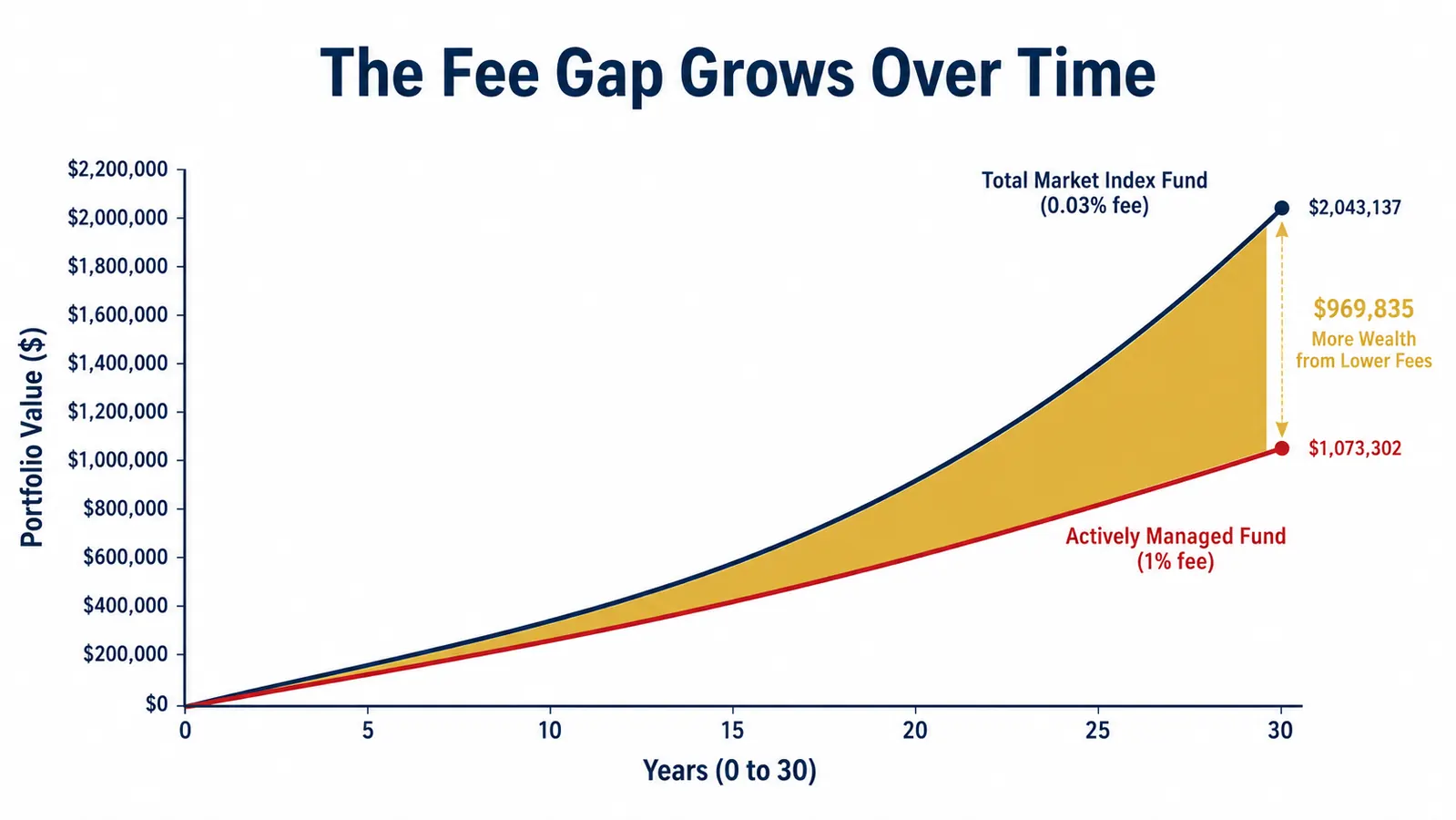

ETFs did not really exist until the late 1990s, and while the 10th anniversary edition adds a chapter on them, the core text was written before ETF investing became as accessible and inexpensive as it is now. When Bogle quotes expense ratios as high as 1.5 or 2 percent as typical, those numbers feel distant today. You can now find index ETFs with expense ratios of 0.03 percent. The principle he is teaching is still correct. The landscape he is describing has shifted.

None of this breaks the book's argument. But it does mean you need to update the numbers in your head as you read. The argument for low-cost indexing is stronger today than when Bogle first made it, not weaker. I just wish the examples felt a little more current.

Bogle teaches you the right question to ask about any investment: what does it cost, and does it consistently beat the index after those costs? Almost nothing does. That question alone is worth the price of the book.

What the Book Gets Genuinely Right

Here is where I have to be straight with my skeptic self: the core argument is correct and it changed how I look at my 401k. Before reading this book, I had three funds selected during my onboarding orientation six years ago. I had never looked at their expense ratios. One of them was 0.72 percent annually. That sounds like almost nothing until Bogle explains that on a $20,000 balance, that fee costs you $144 a year, and because that $144 is not compounding, the real cost over 30 years is dramatically higher than the dollar figure suggests.

After finishing the book, I logged into my 401k portal, found the fund expense ratios, and switched two of my three funds to the low-cost index options available in my plan. One of them was a total market index fund with a 0.015 percent expense ratio. That change took about 15 minutes. I did not need a financial advisor. I did not need an app. I needed to know that the expense ratio column mattered, which the book made undeniably clear.

The other thing Bogle gets right is tone. He is not trying to impress you with complexity or scare you with market volatility. He is not selling you on a system that requires active management or ongoing decisions. His message is essentially: keep it simple, keep costs low, stay patient. That is rare in a space full of people who profit from making investing feel complicated.

Who Will Find This Too Basic

If you have already been investing in low-cost index funds for a few years and you understand why you are doing it, this book is going to feel like a long confirmation of something you already know. There is no advanced content here. No discussion of tax-loss harvesting, no guidance on Roth conversions, no analysis of factor investing or sector tilts. Bogle is making one argument about one strategy, and he is not apologetic about staying in his lane.

Finance enthusiasts and people who enjoy digging into market mechanics may also find the book thin. If you want to understand options, read about dividend investing strategies, or learn how to evaluate individual company fundamentals, none of that is here. Bogle's entire position is that you should not be doing any of those things, and he is not going to help you do them.

There is also a subset of readers who will finish the book feeling convinced but stuck. Bogle explains why index funds beat active management. He does not explain how to open a brokerage account, what to type into the search bar when you are looking for a specific fund, or what to do if your employer's 401k does not offer any index options. That gap is real. Our guide on how The Little Book compares to The Intelligent Investor is a good next stop if you are choosing between classic investing reads.

What Bogle Does Not Prepare You For

The book's silence on a few practical topics surprised me. Asset allocation, meaning how much of your portfolio to put in stocks versus bonds versus other things, gets minimal coverage. Bogle mentions that you might want to hold some bond index funds alongside stock index funds, but he does not give you a framework for deciding the ratio. For a 38-year-old with 27 years until retirement, am I 90 percent stocks and 10 percent bonds? 80/20? The book does not answer that.

He also does not address what to do in the years just before retirement, when your time horizon shrinks and the strategy needs to shift. That is a real planning question, and this book punts on it. If you are in your 50s and starting to think about what your investment mix should look like heading into your 60s, Bogle will not give you much to work with here.

And while the book nods at the emotional side of investing, telling you to stay the course during market drops, it does not spend much time on the psychology of watching a balance drop 20 or 30 percent in a down year. That experience is harder than it sounds when you read about it calmly in a book. The intellectual case for holding is clear. The emotional case is harder, and the book does not prepare you for it well. Morgan Housel's The Psychology of Money covers that territory much more thoroughly if you need it.

What I Liked

- Makes the case for low-cost index investing clearly enough that you actually change your behavior

- Honest about how the fund industry profits at investor expense, with real data behind it

- Short enough to finish in three evenings without losing the argument

- Updated edition adds an ETF chapter that brings the strategy into the modern brokerage landscape

- Bogle's tone is calm and credible, never hypey, which makes the argument easier to trust

- Even readers who already invest in index funds may reassess their fund fees after reading it

Where It Falls Short

- Core argument repeats across too many chapters, testing patience in the middle of the book

- Many examples and fund references come from the 1970s to 1990s and feel dated

- Does not explain how to actually open an account or find specific fund tickers

- Asset allocation guidance is minimal and leaves real questions unanswered

- No meaningful coverage of pre-retirement strategy or how the approach should shift over time

- Too basic for anyone already familiar with index fund investing

The Argument That Actually Landed for Me

For all the things the book does not cover, the central idea stuck. Bogle frames it at one point this way: every dollar of performance that the market returns belongs to investors in aggregate. The only question is how much of that dollar you keep after paying the people who manage your money. A fund charging 1 percent takes a significant slice before you see any return. A fund charging 0.03 percent takes almost nothing. Over 30 years, the difference in ending balance between those two funds, assuming the same underlying market performance, can be tens of thousands of dollars on a modest starting investment.

That framing is not complicated. It does not require a finance degree. It is just math that most people have never been shown clearly. After reading this book, I showed that math to my nephew Darius, who is 24 and just started his first job with a 401k. He spent 20 minutes with it and switched from the target date fund his company defaulted him into to two lower-cost index funds. That is the practical value of this book: it gives regular people a specific thing to look at and a specific reason to change it.

Who This Is For

This book is for you if you have money in a 401k, IRA, or investment account and you have never looked at the expense ratios of what you are holding. It is for you if someone has suggested index fund investing and you want to understand why before you commit to it. It is for you if you are a first-time investor who wants the foundational logic before you start clicking through a brokerage account. And it is for you if you are skeptical that anything this simple could actually work long-term and you need to see the data before you believe it.

My honest recommendation: read it once, take notes on the chapters that hit hardest for your situation, and then find a supplementary resource that covers the practical mechanics. This book will give you the conviction. You will need something else to give you the step-by-step. For readers who want to go deeper on the comparison between index investing and other classic approaches, our piece on a long-term perspective on Bogle's advice in practice covers what applying this strategy actually looks like over time.

Who Should Skip It

Skip it if you are already invested in low-cost index funds and understand the rationale. Skip it if you are specifically looking for guidance on individual stocks, real estate investment trusts, tax strategy around your investments, or any form of active portfolio management. Bogle would tell you to skip all of those things, and his book will not help you do them. Also skip it if repetition frustrates you as a reader. The first 40 pages will say everything the book has to say. The next 170 pages will say it again in different ways.

But if you are sitting with a 401k you have barely looked at, or a brokerage account full of funds someone recommended without explaining the costs, or just a nagging feeling that you should be investing but have no framework for deciding how, this book is a good way to spend three evenings. It will not answer every question. It will answer the most important one.

If nobody has ever explained your 401k expense ratios to you, Bogle does it in plain language in the first three chapters.

The Little Book of Common Sense Investing is not perfect. But it is the clearest explanation available of why low-cost index funds beat most of what the financial industry sells you. Check today's price on Amazon.

Amazon Check Today's Price on Amazon →