For about four years, I read every personal finance article I could find. I budgeted in spreadsheets. I saved up a small emergency fund. I told myself I was being responsible. But something still felt off. Every paycheck would come in, expenses would go out, and I would be left feeling like I was running in place. I was not in debt by most standards. I just was not going anywhere either.

A coworker mentioned Rich Dad Poor Dad by Robert T. Kiyosaki in a casual conversation. She said she had read it twice. I had seen the title on bestseller lists for years and always assumed it was one of those "believe in yourself and hustle" books that would not tell me anything concrete. I picked it up anyway, mostly because I was out of ideas.

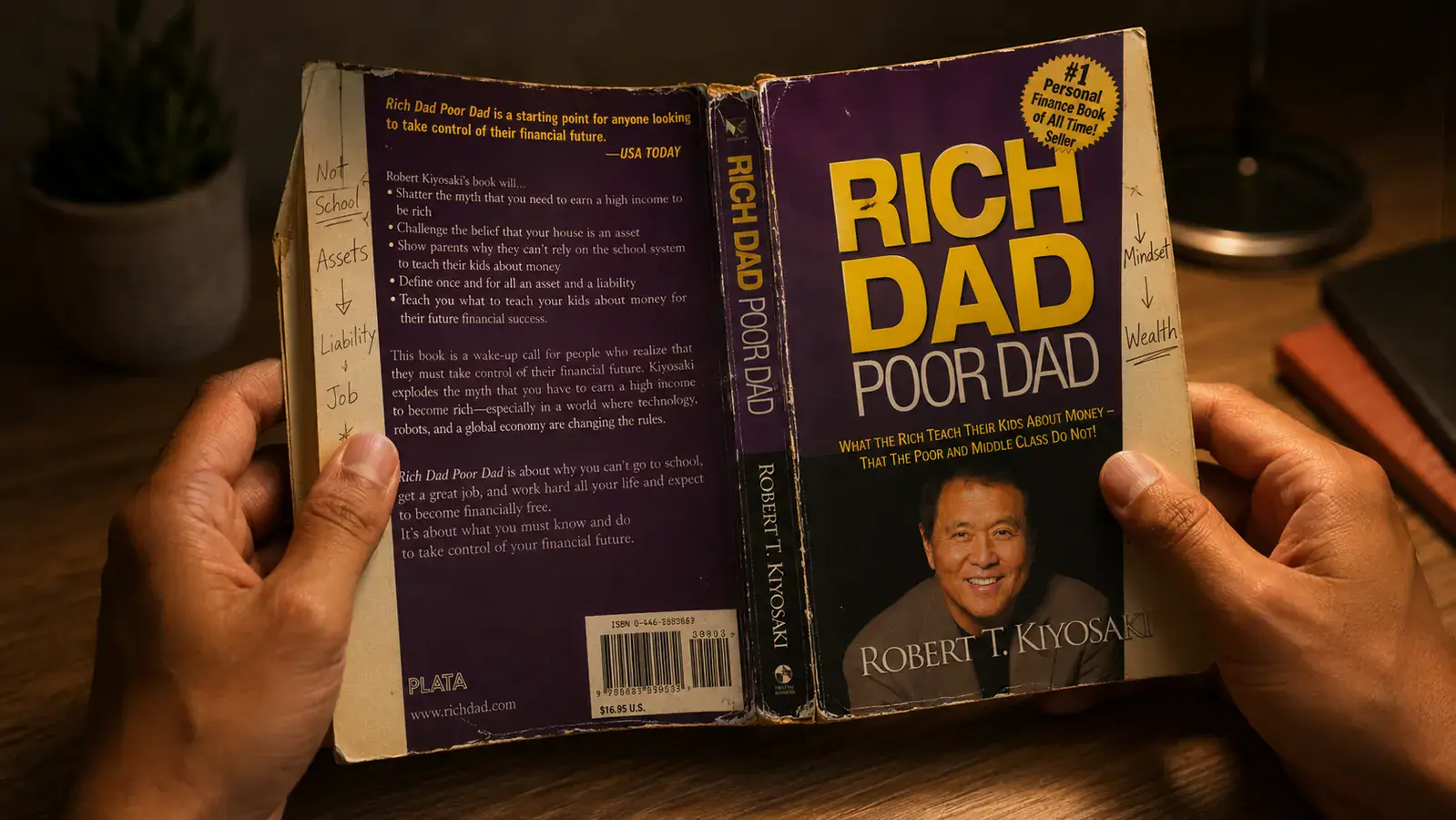

The first half of the book is a memoir-style comparison between two father figures Kiyosaki had in his life. His biological father was educated and hardworking but always struggled financially. His friend's father, the so-called Rich Dad, ran businesses and thought about money in a fundamentally different way. The contrast is drawn through lessons Kiyosaki received as a kid. It reads more like a story than a textbook, which is probably why it has sold over 40 million copies. I found myself reading faster than I expected.

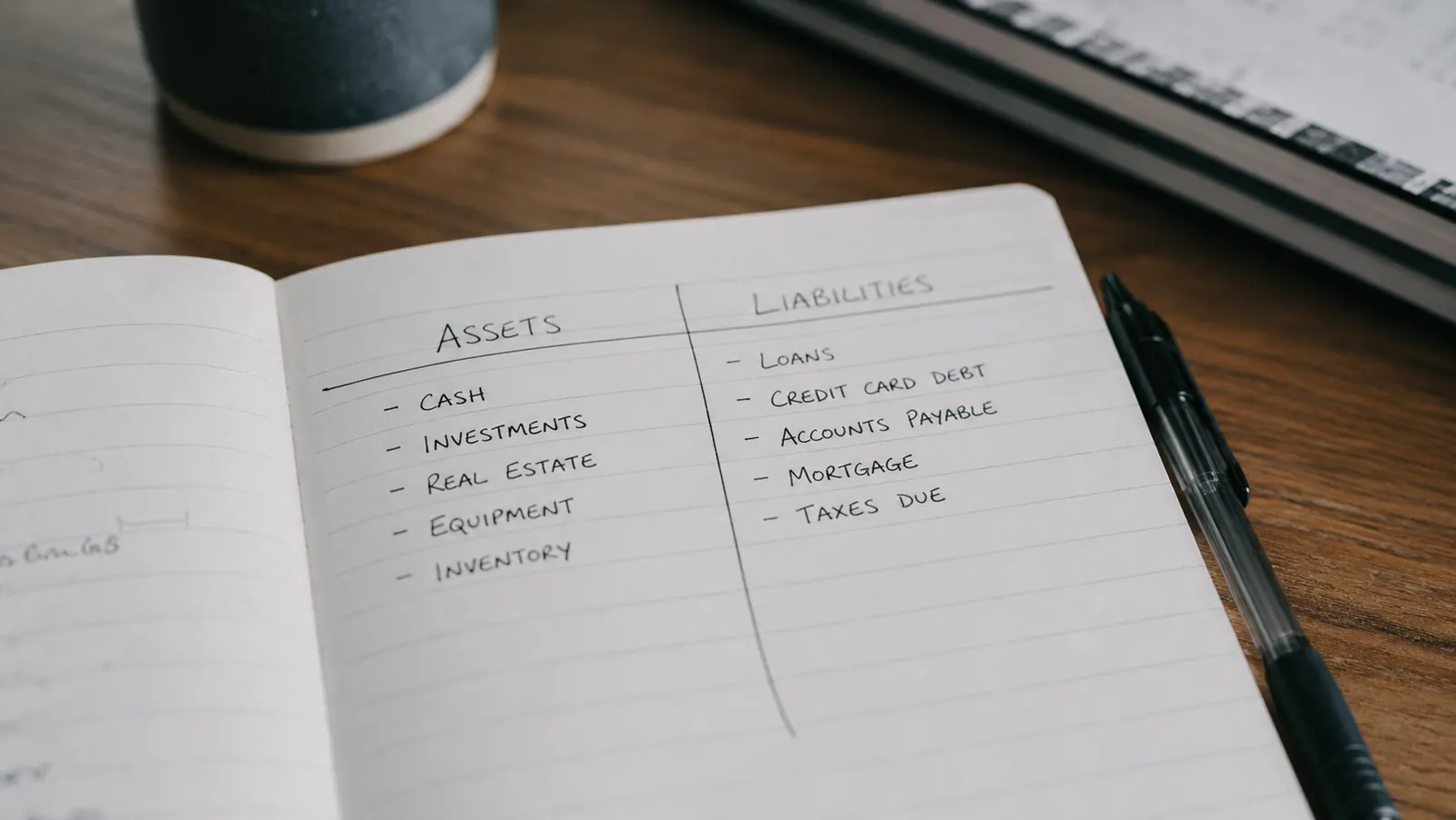

Then I hit a chapter that stopped me cold. It was the explanation of assets and liabilities. Kiyosaki's version of those terms is not the accounting definition most people learn. His is simpler and, honestly, more useful for thinking about your own situation day to day. An asset, in his framing, is something that puts money into your pocket. A liability is something that takes money out. That is the whole distinction. And when I started mentally running through everything I owned and everything I owed, I realized almost nothing in my life was an asset by that definition.

My car took money out every month. My apartment took money out every month. Even the things I thought of as "good" financial decisions, like buying furniture outright instead of on credit, were just liabilities I had purchased in cash. I was not poor. But every dollar I earned was going to things that never paid me back. Kiyosaki calls this the rat race, and I finally understood what that phrase actually meant.

I was not in debt. I was not spending recklessly. But every dollar I earned was going toward things that never paid me back. That one reframe changed how I looked at every purchase after.

I want to be honest about what happened next, because I think a lot of people read this book and then feel either overwhelmed or like they need to go buy rental properties immediately. That is not what I did. I did not have the capital for real estate. What I did was something much smaller. I opened a brokerage account and started putting a set amount each month into a low-cost index fund. That was it. It was not dramatic. But I was, for the first time, deliberately moving money toward something that had a chance of paying me back.

Over the following year I also got more careful about what I called "lifestyle inflation." Every raise I had ever gotten previously went straight into a nicer apartment or eating out more often. After reading this book I started asking a different question before spending money: does this put money in my pocket or take money out? That filter has been more useful to me than any budget spreadsheet I ever built.

Still running the same financial playbook you learned growing up?

Rich Dad Poor Dad has more than 107,000 reviews on Amazon and has been in print for over 25 years. It is not a get-rich book. It is a different way of seeing money, explained through two real-life examples. Worth reading before your next raise goes the same place the last one did.

Amazon Check Today's Price on Amazon →Rich Dad Poor Dad is not a complete financial plan. Kiyosaki does not give you step-by-step instructions for buying your first rental property or calculating your net worth. Some critics point that out and they are not wrong. The book is light on specifics. But I have come to think that is actually fine, because the specifics come later, after the mindset shifts. If you start with the right framework for thinking about money, the tactical decisions become much clearer. If you start with tactics and the wrong framework, you can follow every rule and still feel like something is missing. That was my situation for four years.

I will also say that not every idea in the book landed for me. Kiyosaki is bullish on certain types of assets, particularly real estate and owning businesses, in a way that does not map onto everyone's starting point. Some of his advice assumes you have room to take financial risk, which not everyone does. But the core asset-versus-liability lens is genuinely useful regardless of where you are starting from. You can apply it whether you have $100 to invest or $10,000.

If you want to dig further into the concepts once you have finished the book, the companion article on how to start building wealth from zero using the Rich Dad approach breaks down the practical first steps. And if you want a longer look at the book itself before deciding whether to buy it, the full Rich Dad Poor Dad review covers the content in more depth and explains who gets the most out of it.

What I'd Tell You If We Were Sitting at My Kitchen Table

Here is what I would say to you if you were sitting across from me right now. If you have spent any time feeling like you are doing the responsible things but still not getting ahead, this book might give you the vocabulary for what is happening. It is not that you are bad with money. It is more likely that nobody ever explained which direction money is supposed to flow. That one reframe, assets put money in, liabilities take money out, is worth more than most of the budgeting advice I followed for years before it. You do not need to become a real estate investor. You do not need to quit your job. You just need to start making sure that some of what comes in is going toward things that push something back. That is not a get-rich idea. It is just a more honest accounting of what your money is actually doing. This book started me on that path, and I think it is worth a few hours of your time.

One book, one idea, one shift in how you see money.

Rich Dad Poor Dad by Robert T. Kiyosaki is one of the best-selling personal finance books ever written. Over 107,000 readers have reviewed it on Amazon. It is not magic. But if the assets vs liabilities concept is new to you, it might be the most useful thing you read this year.

Amazon Check Today's Price on Amazon →