I read Rich Dad Poor Dad for the first time in my late twenties. I was working full-time, carrying about $11,000 in credit card debt, and doing exactly what I had been told to do: show up, work hard, and hope the next raise would finally fix things. A coworker handed me her copy and said it had changed how she thought about money. I read it in two evenings, felt fired up for about a week, and then put it on the shelf. Nothing changed. Nine years later, I read it again. This time, things landed differently. That gap matters for this review, because who you are when you pick up this book determines almost everything about what you get out of it.

Rich Dad Poor Dad by Robert T. Kiyosaki has been in print since 1997. It has sold over 40 million copies. It has also attracted genuine criticism from financial planners who call it vague, from journalists who have questioned whether the titular "rich dad" was a real person, and from people who followed the real estate advice at the wrong time and got hurt. I want to address all of that honestly, because this is a book that deserves a clear-eyed look rather than either cheerleading or dismissal.

The Quick Verdict

A genuinely useful mindset shift for people who have never questioned how money works, undermined by thin specific guidance and a real estate focus that does not apply to everyone.

Amazon Check Today's Price →Still paying rent and wondering why your savings never grow? This book names the pattern.

Rich Dad Poor Dad reframes how you think about income, assets, and the work-to-spend cycle. It is not a step-by-step plan, but for many readers, it is the starting point that finally made the other books make sense.

Amazon Check Today's Price on Amazon →How I Have Used It (And Misused It)

The first time I read this book, I treated it like a manual. I highlighted everything. I made a list of "assets I want to acquire." I looked up rental property prices in my area. Then I looked at my savings account and felt defeated, because I had nothing close to a down payment and no idea how to get there. The book had inspired me without actually telling me what to do next. That gap between inspiration and instruction is real, and it is worth naming upfront.

The second read, nine years later, I was in a different spot. I had paid off the credit card debt, built a small emergency fund, and started contributing to my 401(k). I was financially stable but still felt like I was just running on a treadmill. This time, the book hit harder, because I could see the pattern Kiyosaki describes in my own life. I was earning more than I ever had and still not building anything. The asset-versus-liability framework gave me a language for what I had been feeling but could not articulate.

Over the past year, that framework has shaped small, real decisions. I stopped upgrading my car when the lease came up and kept the paid-off one. I redirected what would have been a car payment into a low-cost index fund. I started a small side project that earns a few hundred dollars a month and reinvested that back into the same fund. None of that is dramatic. But the mental shift behind it started with this book.

The Core Idea, Explained Plainly

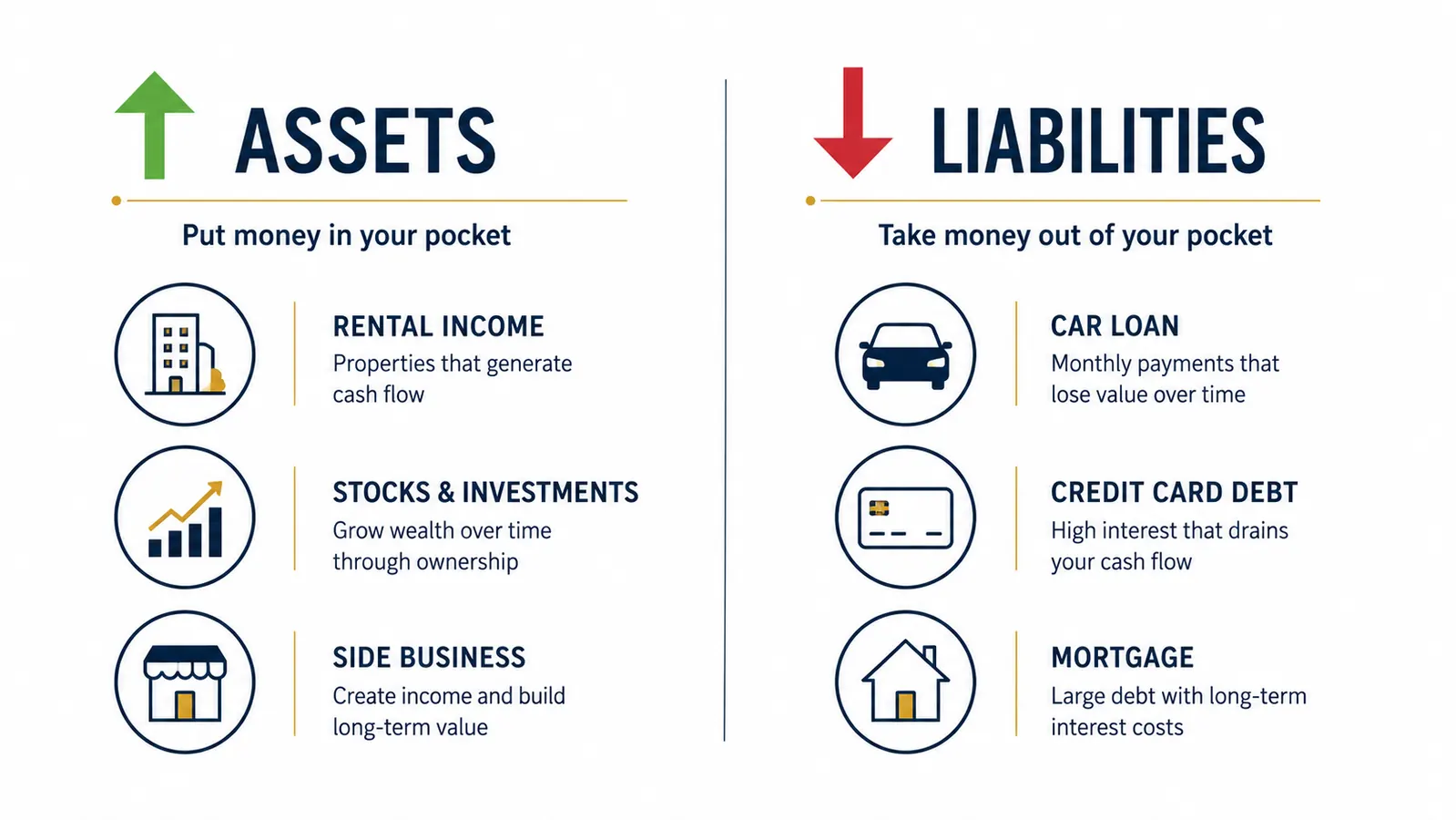

The book's central argument is this: most people trade time for money their whole lives, then spend that money on things that cost them more money. Rich Dad calls this the "rat race." The alternative is to acquire assets, meaning things that put money into your pocket regardless of whether you are working. Kiyosaki's favorite examples are rental real estate, stocks that pay dividends, and small businesses. The contrast he draws is between his biological father (educated, well-paid, but financially stressed his whole life) and a friend's father (less formally educated, focused on building assets, eventually wealthy).

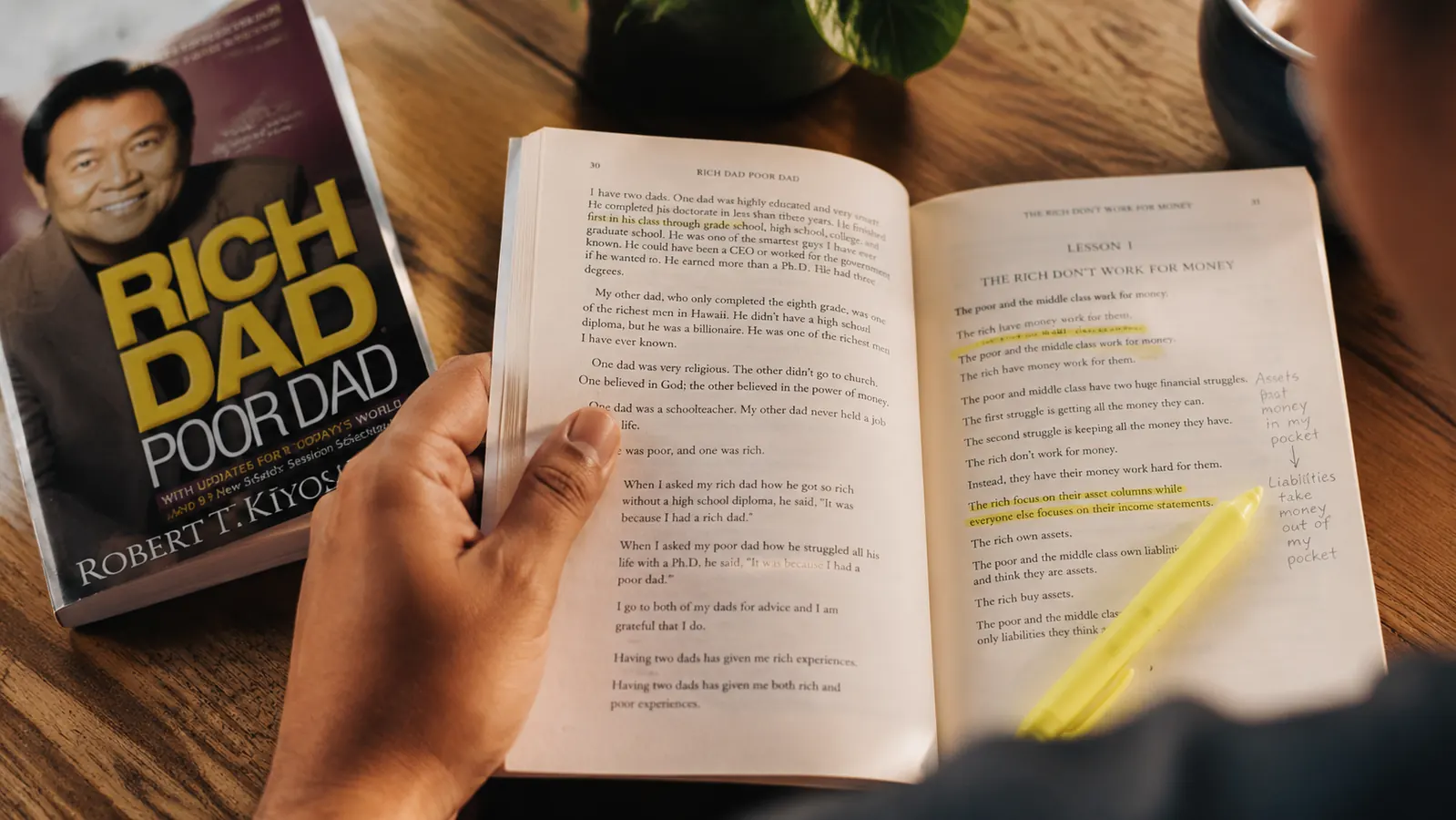

The assets-versus-liabilities distinction is where the book earns its reputation. Kiyosaki makes a point that sounds simple but takes a while to really absorb: your house is not an asset if it costs you money every month. Your car is not an asset. Your flat-screen television is not an asset. Assets produce income. Liabilities consume it. Most of us have been taught to call things we own "assets" simply because we own them. That reframe alone is worth the read.

The question the book asks is not how much are you earning but what does your money do while you sleep. That is the shift. I had been answering the wrong question for a decade.

What the Book Gets Right

The emotional diagnosis is accurate. Kiyosaki is describing something real: the pattern where educated, well-paid people feel financially stuck because their spending rises with their income and nothing ever accumulates. He calls this "lifestyle creep" before that phrase was common. He frames it as a systems problem, not a willpower problem. That is the right frame, and it is genuinely different from how most personal finance books position the issue.

The book is also right about financial literacy being undervalued. Kiyosaki's frustration with how schools handle money, or do not, is legitimate. Understanding basic concepts like cash flow, compound interest, and return on investment is not taught consistently in K-12 education, and most people arrive at adulthood without this foundation. The book plants that frustration in the reader in a useful way, motivating them to learn more.

The chapter on taxes is underrated. Kiyosaki explains that corporations pay taxes on what remains after expenses, while employees pay taxes before they can spend anything. That is a real structural difference, and it is one that most people have never had explained clearly. He is not telling you to incorporate your life or avoid paying taxes. He is pointing out that understanding the rules of the system you are operating in gives you more choices. That was new information for me the first time I read it, and it still holds up.

And the asset-building mindset, even applied modestly, works. I am not buying rental property. I do not have a business empire. But thinking about each financial decision in terms of whether it builds or drains has quietly improved my balance sheet over the past year. That is the real practical value here, not the specific vehicles Kiyosaki recommends, but the habit of asking the right question before spending.

Where It Falls Short (Honestly)

The book is light on specifics. When Kiyosaki says "acquire assets," he usually means rental real estate, but he rarely walks through how someone with minimal savings actually starts that process. The advice lives at a conceptual level, which is frustrating if you are looking for a plan. You will finish the book motivated but possibly unclear on what your literal next step should be. That is not a small gap.

There is also the credibility question. Over the years, journalists and financial critics have pushed back on Kiyosaki, questioning whether the "rich dad" story is literal biography or a teaching narrative, and noting that his company filed for bankruptcy in 2012 amid a legal dispute. He has also made investment calls, particularly around gold and Bitcoin, that have been controversial. None of that means the core ideas in this book are wrong. But if you are evaluating someone's advice, their track record matters, and Kiyosaki's is mixed. Take the framework seriously. Take specific recommendations from this book with more skepticism.

The real estate focus can also feel dated or inaccessible. In the markets where most readers live today, entry-level rental properties require significant capital and carry meaningful risk. Kiyosaki wrote much of this book in the 1990s when real estate dynamics were different. The asset-building principle transfers, but the specific vehicle he favors most does not translate cleanly to every reader's situation or geographic market.

Finally, the tone can feel condescending toward people who choose employment over entrepreneurship. Kiyosaki is dismissive of people who find meaning and security in good jobs. Not everyone is built for, or interested in, running a business or being a landlord. The book sometimes reads as if those people are making a failure of character rather than a considered life choice. That framing is not fair, and newer readers may find it off-putting.

What I Liked

- The assets-versus-liabilities framework is genuinely clarifying and not something most people get taught anywhere

- Makes a compelling case that financial literacy is a skill gap, not a character flaw, which is an important reframe

- Written accessibly. No jargon. Reads fast. You can get through it in a weekend

- The emotional diagnosis of the rat race is accurate and will resonate with most working adults

- The mindset shift it creates transfers to any asset type, not just real estate

Where It Falls Short

- Thin on specifics. You will not find a step-by-step plan here

- Heavy real estate bias that does not apply cleanly to most readers' situations today

- Kiyosaki's own track record is mixed, and some of his specific investment calls have aged poorly

- The rich dad character's story may be more parable than literal biography, which undermines some of the trust

- The dismissive tone toward employees and traditional careers feels preachy at times

How the Mindset Applies Without Buying Real Estate

This is the part of the book that tends to get lost in both fan summaries and critic responses. Kiyosaki's specific asset recommendations, real estate, small business, commodities, are not the point. The point is the question he teaches you to ask before any financial decision: does this put money in my pocket, or does it take money out? Apply that question consistently, and the vehicles almost do not matter. Index funds are assets. A paid-off car with no payment is a mild asset compared to a lease. A skill that lets you take on freelance work is an asset. Even a high-yield savings account, modest as it is, is moving in the right direction.

One practical test I started using after my second read: before any purchase over $200, I ask myself whether this item will be worth more or less in two years, and whether it generates any income in the meantime. That test kills a lot of unnecessary spending without requiring discipline or budgeting willpower. The item either qualifies as an asset or it does not. That simple filter, which came directly from this book, has probably saved me several thousand dollars in the past twelve months. Nothing Kiyosaki describes requires a large income or a real estate license. It requires a different way of looking at spending.

After my second read, I paired this book with a simple index fund account and a side project that takes about five hours a week. Those two moves did not come from this book directly. But I would not have pursued them without the mental reframe that the book gave me. It changed the question I was asking, from how do I earn more to how do I build something that earns without me.

Who This Is For

This book is best for someone who has never seriously questioned the earn-spend-repeat cycle, who feels like they work hard but never get ahead, and who is ready to consider that the issue might be structural rather than a willpower problem. If you have been meaning to "get better with money" but have not found the motivation to change anything yet, this book tends to light that fire. It is also a solid read for anyone who has handled the basics (debt paid down, emergency fund started) but still does not have a clear picture of what they are building toward. The mindset layer is where this book earns its keep. If you find the ideas here interesting, a natural next step is our roundup of ten specific money lessons from the book, which walks through the framework in more practical terms. You can also read how it compares to Dave Ramsey's approach if you are trying to decide which philosophy to start with.

Who Should Skip It

If you are already financially literate and looking for tactical guidance, this book will frustrate you. It is not a step-by-step plan. If you are in a debt crisis and need concrete help with budgeting and cash flow, something like Dave Ramsey's Total Money Makeover will serve you better right now. If you want a more nuanced and modern take on how psychology affects financial decisions, Morgan Housel's The Psychology of Money covers some of the same emotional terrain with better specificity and fewer credibility concerns. Rich Dad Poor Dad is a mindset book. If you need a tactics book, look elsewhere first, then come back to this one.

If you still think working harder is the answer, this book will challenge that assumption.

Rich Dad Poor Dad has been in print for nearly 30 years and sold over 40 million copies. The core framework, assets versus liabilities, is genuinely worth understanding, even if you ignore the specific investment advice. Check current pricing on Amazon below.

Amazon Check Today's Price on Amazon →